Do You Need to be Concerned About Rising Inflation?

August 5, 2021 - 4 minutes read

Posted by James Spencer

As the UK Government takes its next steps on the Coronavirus recovery plan, there is no way to predict how the economy will fare through these unprecedented times. What we do know is that inflation is rising for the first time in years – though this isn’t necessarily something to worry about.

Here, Financial Planner Ed Stubbs explains what we know about the rise in inflation and how it may impact interest rates, assets, and investments – but most importantly of all, your financial plan.

The global impact of Covid-19 could easily have become a grave financial crisis if not dealt with carefully by governments around the world, especially given the global economy hadn’t fully recovered in many ways since the 2008 financial crisis. The response to Covid-19 has been similar in some ways to 2008 (albeit not all), when the UK, US, and EU governments and central banks injected funds into their respective economies, just on a much larger scale than before.

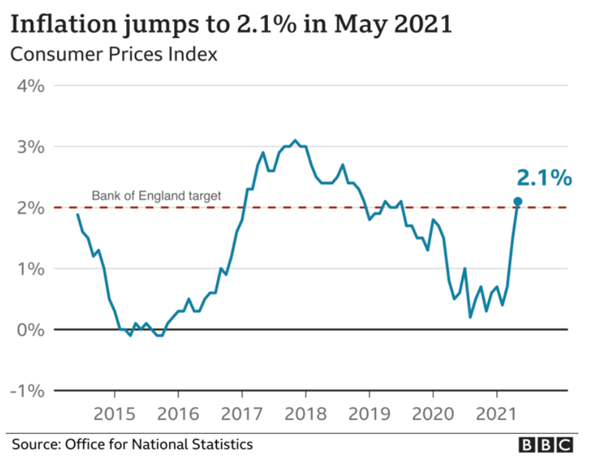

Over time inflation will consistently undercut the value of savings and investments, with money tending to halve in value every 10-12 years. The period from 1970-1982 famously saw regular double-digit increases year-on-year. From 1993 onwards, inflation has been relatively low and stable, ranging between 0.37% to 3.86%. As the Coronavirus pandemic hit global and national economies last year, inflation has been on the rise. In May, the consumer price inflation (CPI) rate hit a two-year high of 2.1% in May 2021, surpassing the Bank of England’s 2% target, with predictions of further rises to come.

(Source: BBC)

Due to global supply and trade complications and increased illness/self-isolation, products and services are in short supply and as lockdown restrictions continue to ease, people will continue spending the money that the UK government has injected into the economy. The combined impact of these events means there is a lot of money circulating for limited products and services and people are willing to pay more since products are in high demand.

Historically, such a rise in inflation would have encouraged the Government and Bank of England to consider increasing interest rates, to reduce the demand for goods and services. However, up to now, they have decided to hold steady and watch how the market develops.

According to the Monetary Policy Committee, this period of high inflation is expected to be “transitory” and hasn’t yet reached the point where the bank needs to react with higher interest rates to dampen the economy. Therefore, the MPC in June voted 9-0 to keep interest levels at the record low rate of 0.1%, as they have been since March last year when they were dropped to help absorb the impact of the pandemic.

The Bank of England’s Monetary Policy Committee (MPC) has stated it expects the rate of inflation to rise above 3% for “a temporary period”, as these issues filter through the economy, but some observers are not so sure how temporary this may be. There are a number of competing effects that will continue to help to soften any increase though, including the deflationary effects of technology and the UK’s demographic shift to an aging population.

Most experts agree about the need to avoid sustained and significant inflationary increases, which will create instability and impact investors and savers across the board, but the Bank of England is walking a fine tightrope between dampening down inflation and causing instability elsewhere, given the high amounts of government, corporate, and personal debt across the financial system.

In some ways the government would welcome a rise in inflation as it will allow them to account for some of their debt, meaning they can avoid raising taxes or cutting spending.

And investors with asset-backed investments can also sometimes benefit from a little inflation. For example, between 1987 and 2015, retail prices rose by approximately 155%. However, over the same period, UK shares had risen by 294%.

The Impact on You

Whilst it is important to be aware of what’s happening with inflation and the potential consequences for future interest rates, the most important consideration for us is whether each of our family’s financial plans is on track. All financial plans are individual – one family’s concerns over rising private school fees could be juxtaposed with another family’s delight at lower debt costs for their business. Equally, temporary inflation is not as much of a worry for someone who knows they can comfortably maintain their desired income through age 100, even if asset prices lag inflation figures for a year or two.

As you can see, the impact of inflation will vary from family to family according to their goals and circumstances. Overall, however, we always take a long-term view over investment strategy, finding value where we can whilst ensuring the defensive element of our portfolios is robust enough in times of market instability. A solid WealthPlan™ strategy will always stand you in good stead so you can hold firm to your financial goals and control the controllable, regardless of what happens to inflation and interest rates.

This is a topic that we’re discussing at many of our annual reviews recently, but if you would like to discuss any aspect of financial planning in the meantime, please do get in touch.

About Ed

Ed is a Financial Planner who joined Xentum upon graduation in 2014. He specialises in the creation and delivery of financial plans that help our families to live life to the full, free from financial worry.

Contact: Ed.stubbs@xentum.co.uk; 01925 398338.