New Tax Year – What’s Changed?

April 1, 2022 - 4 minutes read

Posted by James Spencer

The new tax year is just a few days away and so it makes sense that we’re all talking about – you’ve guessed it – tax.

The new tax year is just a few days away and so it makes sense that we’re all talking about – you’ve guessed it – tax.

The new tax year is just a few days away and so it makes sense that we’re all talking about – you’ve guessed it – tax.

The new tax year is just a few days away and so it makes sense that we’re all talking about – you’ve guessed it – tax.The big topics right now are changes to National Insurance and dividend tax, explains Craig Watts of Redstone Accountancy Services, a company we have worked closely with for a number of years.

The Chancellor announced his Tax Plan in March’s Spring Statement, including an increase to the threshold for National Insurance (NI). But how does this all fit in with the planned increase to NI rates announced last September? And what if you receive your income through dividends?

Let’s start with what you need to know about NI:

Employing staff and taking salary from your business:

The threshold for paying NI will be aligned with the personal allowance from July 2022. This will mean employees pay less NI on their income. NI will be paid on income over £12,570 (increased by around £3k) from this date. The change is expected to save employees over £330 per year. The rate of income tax is planned to be reduced from 20% to 19% in April 2024 provided the UK meets its economic targets.

The rate of employment allowance given to employers with more than 1 member of staff will increase from 6th April 2022 by £1,000. This means employers’ NI bills will be reduced by £1,000 next tax year.

Self-Employed Individuals:

From April 2022, self-employed individuals with profits between the Small Profits Threshold and Lower Profits Limit will continue to build up NI credits but will not pay any Class 2 NICs. This will ensure the first £12,500 earnt is tax-free.

From July 2022, the Lower Profits Limit will be aligned to the personal allowance of £12,570 (to be on par with employed individuals).

But what about the NI rate going up?

When it comes to the planned hike in NI, Mr Sunak has said that this will go ahead as planned as a “dedicated funding source” for health and social care.

This new Health and Social Care Levy is being introduced this month. It will be added to your NI bill, if you earn enough to pay NI. The hike in NI of 1.25% points a year from April 2022 is earmarked to help the overstretched NHS and “equivalent bodies across the UK”.

This means employees will see their NI contributions increase from 12% to 13.25%, while employers’ contributions will jump from 13.8% to 15.05%.

The Health and Social Care Levy will be paid separately to NI contributions from April 2023.

However, Mr Sunak is quick to point out that the NI threshold increase “ is the largest increase in a basic rate threshold ever, and the largest single personal tax cut in a decade.”

Christine Cairns, tax partner at PwC, commented that “increasing the threshold was one of the only options left to try and soften the blow for those who will feel it most.”

“While it might seem curious to be effectively both increasing and cutting NI at the same time, today’s change is clearly targeted at helping those with the lowest earnings who may already be below the income tax threshold.

“The true impact of this cut, as well as of the future decrease of the basic rate tax rate, for middle-income earners will need to be assessed against the impact of the freezing of the income tax bands until 2026,” she said.

IFS director, Paul Johnson tweeted “…. What is the possible justification for cutting income tax rate while raising NI rate?…”

The NI debate certainly has people divided and this announcement does feel like an attempt to reverse some of the impacts the planned NI hikes will have. Is this just a measure being brought in to prevent any U-turns on the plans set out in September? It certainly seems possible.

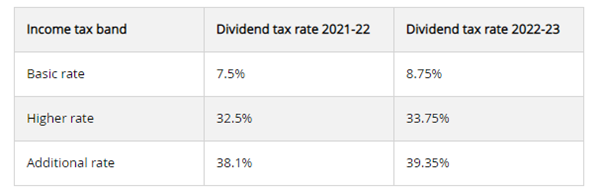

What about dividend tax?

As we now know, plans are going ahead to increase NI contributions for the employed but what about those who receive their income through dividends? It was announced in the Autumn Budget that dividend tax is due to increase by 1.25% for all dividends received from 6th April 2022 onwards. As per the NI increase, the increase to dividend tax will go towards the new Health and Social Care Levy. The government says it hopes to raise £0.6bn from the increase in dividend tax rates.

So, what does this look like?

There are currently three bands of dividend tax, which are increasing as follows:

Within a company’s accounts, dividends are treated differently than salary. Salaries are tax-deductible for the company and reduce the amount of Corporation Tax payable. Because there is no NI ( currently) on investment income, paying dividends is usually a more tax-efficient way to extract money from your business, rather than taking a salary.

At Redstone, we will look to find ways to help increase the tax efficiency of our clients’ remuneration packages. Over the years, the efficiency of this planning has somewhat reduced and the announced increase in the dividend rates narrows the gap even further.

Dividend tax is complex and everyone’s position will be different, so it’s important that you look at your entire income situation to enable you to make the right decisions. If you have a question about any aspect of the changes, or would like to review your tax situation, please get in touch with a member of the Xentum team, or contact Redstone.