Not Your Usual Bucket List

December 7, 2021 - 5 minutes read

Posted by James Spencer

Soon we are closing the door on another year. Are you thinking about all the things that you wish you could have done but didn’t? Thankfully, 2022 is the opportunity to review not only your life goals but also your financial ones.

We all have that proverbial “bucket list” clunking around in our heads, filled with places where we want to go or the adventures we want to experience. But what if we told you about another bucket that illustrates the means to allow you to check off this dream list?

As Paul Armson explains in his book, ‘Enough? How Much Money Do You Need For the Rest of Your Life? ‘, we all could do with sitting down comfortably, pen and paper in hand, to do a basic calculation of what we have and how to make it work for us.

Working out your worth

We are here, not simply to talk about your money, but to work with you to create a lifestyle financial plan which will help you make your goals into reality. The great thing about this approach is that it automatically helps you make better decisions and alleviates stress or worry about your future. The best starting point is calculating the cost of your existing lifestyle and understanding how money flows into and out of your wealth ‘bucket’.

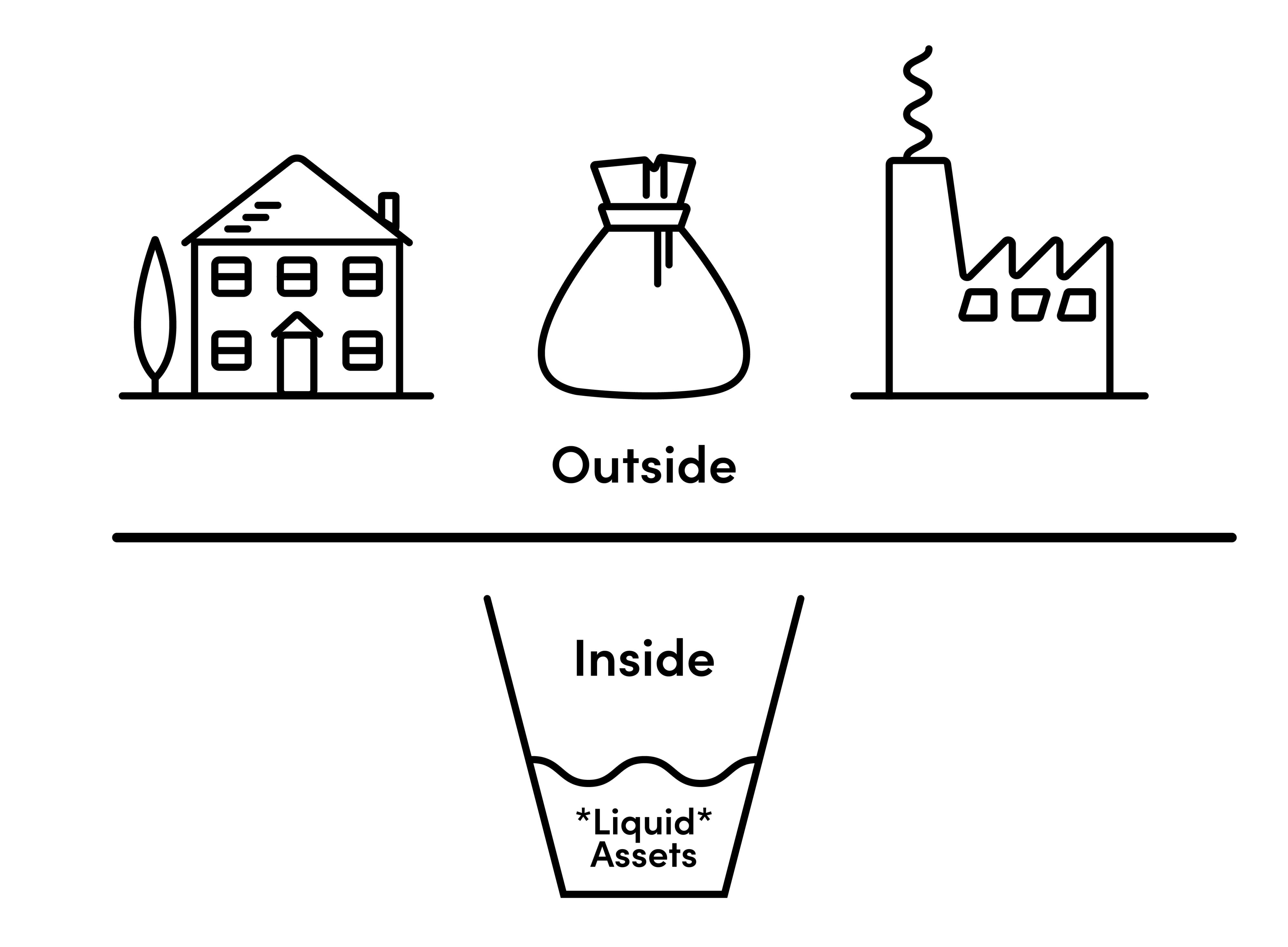

Pour in your liquid assets

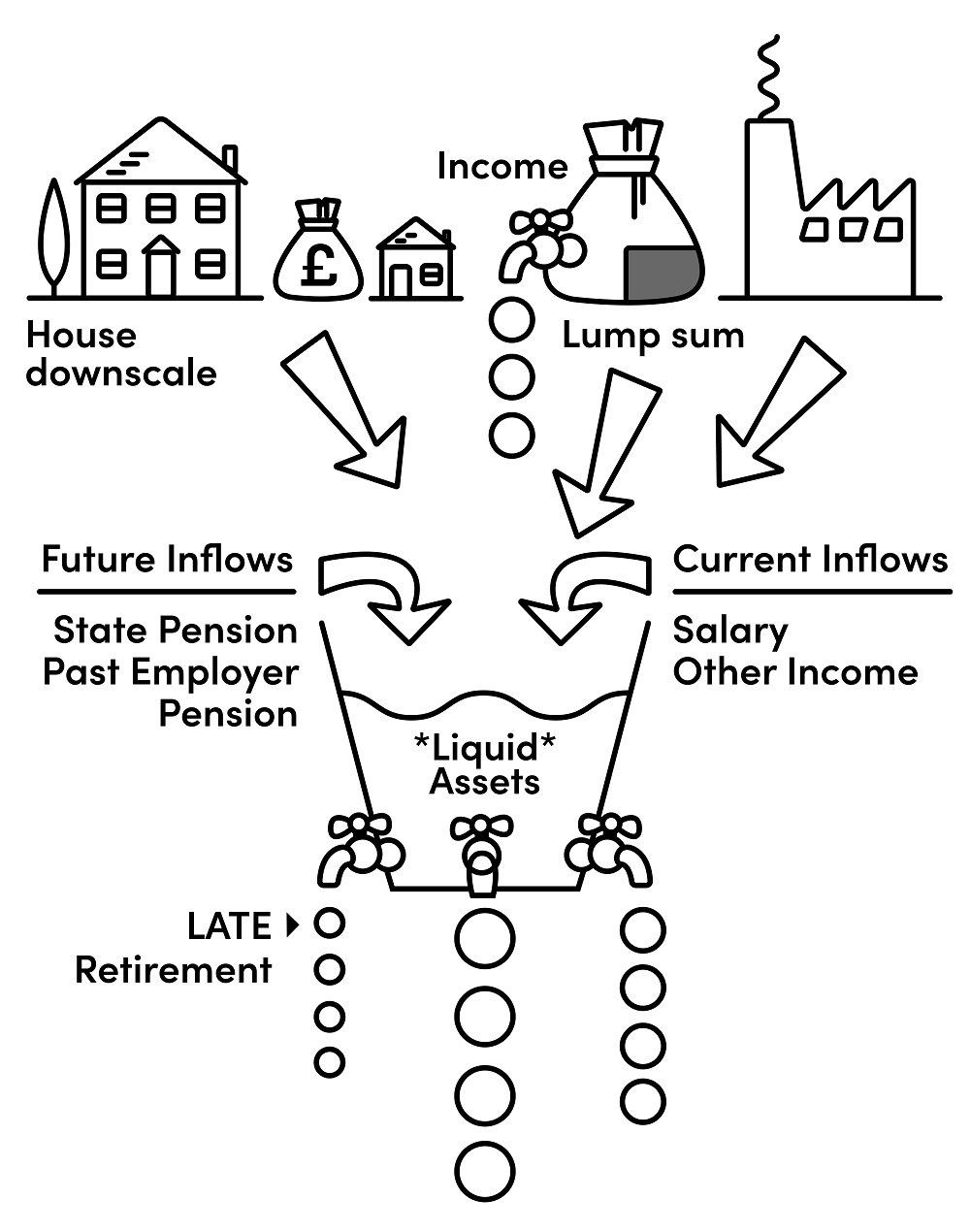

So, let’s imagine an empty bucket. The first thing you want to put in there are your liquid assets. This is money that is readily accessible – savings and current accounts, cash value of ISAs, shares, unit trusts, investments bonds – in other words, things you can easily cash in within seven to ten days. While you are at it, throw in those banknotes and coins in your wallet or at the bottom of your handbag.

Go with the flow

Finances and assets are never static. You are probably still generating income if you are working or sharing your partner’s salary. Armson considers these “current flows” (or income) which we can continually add to the bucket. Included with this are dividends, rental income, bank interest and child benefits, for example.

Can you shift your fixed assets?

Over the years, you will have accumulated other assets which are not as easy to convert to hard cash. Your money is represented in physical things such as your house, your car, your business, or your pension plan. For example, you can’t take your front door and trade it in at your local supermarket for your weekly food shop!

To add these fixed assets to your bucket, they would need to be liquidated – if this falls in line with your lifestyle financial plan.

For example, you may decide in the future to downsize your home. The difference in value between your current house and the next house you purchase becomes another Liquid Asset to add to the bucket. This may be 20 years from now or 10 years from now.

If you are a business owner, until you sell that business (or second property), and deduct any expenses and taxes involved, it will have to remain outside of the bucket.

If you are a business owner, until you sell that business (or second property), and deduct any expenses and taxes involved, it will have to remain outside of the bucket.

When is your pension really YOUR money?

Another fixed asset is your pension fund. Though we think it is ours, it really isn’t until we reach a certain age. In the UK, you can access this fund when you reach 55 but will suffer tax implications. The current retirement age for both men and women in the UK is 66, due to rise to 67 by 2028 and most likely will climb from there.

In summary, pensions and fixed assets remain outside of our illustrative bucket until we choose to draw income from them. We can consider these “Future Inflows.”

What goes in, must come out

Now that we have a timescale for your liquid and fixed assets, you can now face the truth of your expenditures. Imagine there are three taps at the bottom of the bucket.

The first tap deals with your current lifestyle. Every time you use your credit card, pay off the monthly household bills, pay for your children’s education or book a summer holiday, these expenses will inevitably drain your current income stream.

When you retire, the second tap will then be turned on. Your living expenses will be as before, supported by your pension income and current liquid assets. This is when you may travel to an exotic location or take up skydiving lessons while you are healthy enough to do so. But with this comes a cost. Other “one-off” costs to consider are a child’s wedding or a new car.

Eventually, you will reach a point when you cannot physically enjoy life to its fullest. You may have complicated health issues that limit your movements. This is when the third, and last tap, will turn on. If you have planned your finances according to the life plan developed years earlier, you should be comfortable with the knowledge that your future retirement income will cover your care.

How Xentum can help you

Gaining clarity on your current and future worth as well as your lifestyle goals is what the team at Xentum specialise in. We use a tried-and-trusted methodology, WealthPlan™, and a sophisticated cashflow modelling software to give you a long-term picture of your income vs expenditure.

You can find out more about WealthPlan™ and our approach here. Alternatively, you can book an exploratory call with a member of our financial planning team. They will be happy to talk to you about how we can help you create a financial plan that’s right for you and your family.

In the meantime, please do download or request a copy of Enough? by Paul Armson which details the bucket concept as described above. The book includes a foreword by our CEO, Dominic Baldwin. This is an excellent short read and a great start to thinking about your own financial priorities.