Why don’t I want to deal with my money?

February 8, 2017 - 7 minutes read

Posted by James Spencer

I have spent a long time pondering this question for a while:

“Why don’t I want to deal with my money”

It is a really important question to me as I deal with people’s finances for a living.

What do I mean?

I don’t like looking at my online banking. I don’t enjoy reading paper statements of what I have spent and I certainly don’t like dealing with financial services in general from banks to the insurance companies that hike my prices for being loyal (yes that one grinds on me).

I know some people enjoy looking at their bank statement and investments every day, but I am not one of them. This particular blog is probably not for you if that is the case.

As I say, I have been pondering this question for a while and I think I have my own answer. It isn’t an answer I am particularly proud of but I am going to be honest:

“I feel like I should have done better with my money”

Do you ever get that feeling? Well here is someone who has dealt with money from the age of 16 and a professional opening up that I don’t feel I have done enough so far. This is the whole purpose fir creating Genius with Money. Most of it is self confession to the mistakes that I or clients have made with money and also the view from underneath the filthy bonnet of Financial Services.

2016 was a year of reality for me. It was time to step up and do something about it. I will tell you some of the steps that I took that have helped. This is me opening up and you may or may not see some of yourself in any of these:

I started to include and empower my wife with the family finances

Many people within the financial services industry look down on me for this, but I don’t care. I find it incredibly difficult and stressful to manage the family finances in addition to other people’s money. I believe this is because I take my job very seriously and it is difficult sometimes to deal with your own finances when you have spent the week looking after other people’s.

This is why I started to involve my wife more in the family finances. Up to the start of last year, I had always taken the burden of money and done ok, but I started to open up about the family finances early last year and to be honest, I haven’t looked back.

My wife now looks after the household budget that we have set together and I don’t tend to get involved with the day to day spending. If I am told to go to the supermarket to get the “big shop” I do it.

This has been a gamechanger for me and has actually freed up a lot of headspace that I didn’t have. Also, my wife has enjoyed the responsibility and is also better at saving money than me. I am a sucker for Amazon Book Recommendations.

If you don’t include your partner in the family finances at the moment and you have a stressful job like running a business, then I would urge you to start talking about it with them and see if they can take any of the burden off you. You might be surprises that it could actually end up in more growth once you have a better frame of mind.

I automated most of my money

Money for me personally is a burden. I don’t particularly enjoy dealing with it and I understand that companies play games to try to make you part with it. I have never been motivated by money but I understand that I need it to achieve what we want as a family. It is incredibly important and that it why I needed to do something to help.

As i said earlier, I can’t stand looking at my bank online. It never feels good enough. That is why I now automate most of my money. I will explain how:

- I get my income paid into one bank account – First Direct

- All my bills are paid from this (including utilities, phones etc..)

- On the 25th of every month we put an allowance on to one of our Monzo cards to pay for food and drinks and any other household items for the month. This is is to last for a month.

- We then have personal Monzo cards we put our discretionary allowance into

- My pension comes from the company as an employer contribution so I don’t have to touch/deal with

- We currently save around 30% of our income into a First Direct Savings account/ISAs as a standing order

- We have standing orders for the kids Junior ISAs setup

And that is it.

It is all setup so that I don’t have to really bother with it, think about it or touch it. Sometimes we will have a big single expenditure that we may need to dip into our savings or bank accounts for but we discuss that now and to be honest I leave that to my wife now.

I wrote about this in more detail in my most popular blog to date – how to plan your income.

I can’t stress how important it is plan and automate.

I built “our” financial plan

This is what I do for a living. I dig into people’s dream and help to build financial plans to help make dreams a reality. It sounds a bit wishy washy but it is amazing how powerful having a purpose with your money and finances is. It makes people change their financial behaviour and I can tell you that people don’t like changing their financial behaviour. Have a think about how many people with negative net worths buy the new Iphone every year. It is because we are not as clever as the companies that market to us every day.

To change your behaviour, you need a purpose and a plan.

I have never said this openly before but my dream is to spend time in other countries with my family while the children are young. I don’t really mean holidays, I mean renting a place out for 5-6 weeks on airbnb and spending time learning other cultures and foods and ways of living.

It was really important that this was put into a plan as it is something I have wanted to do for years. My wife also had things she wanted to do that we needed to incorporate. Once we built our requirements, we then put our current financial situation into a financial forecasting software that I use every week at Xentum and we built our financial plan over a coffee in our local town.

It showed that our financial “wants” were more achievable than we expected and that it just took a slight shift to a more growth mindset in the next 12-18 months.

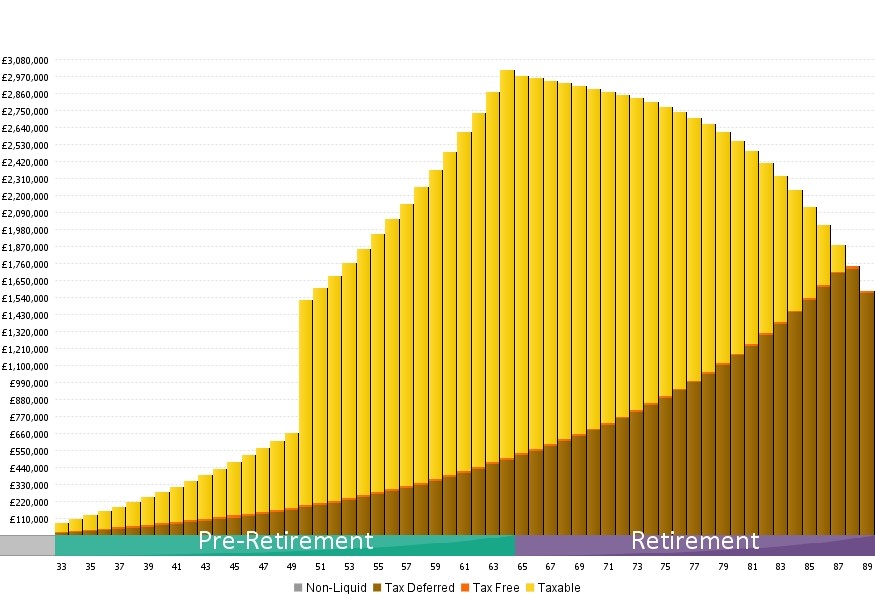

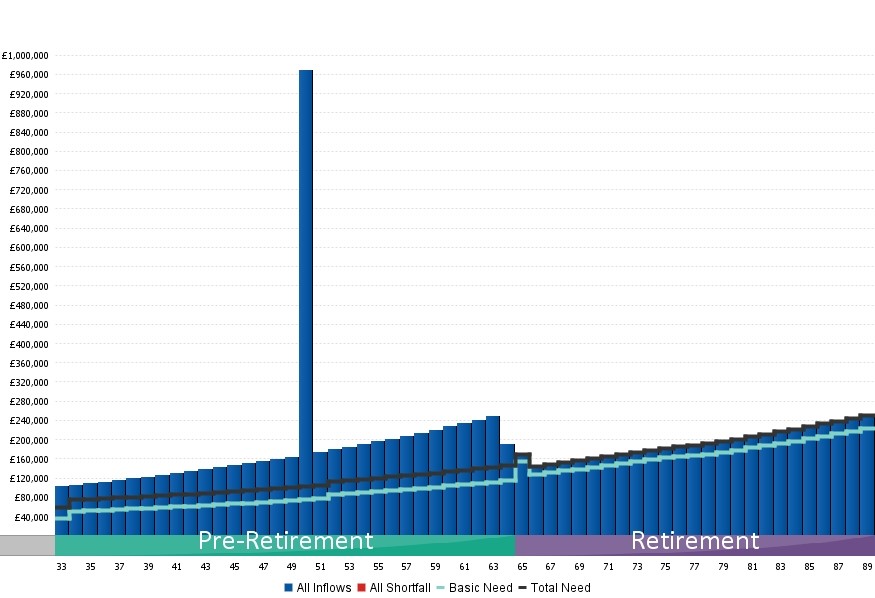

Have you ever seen a business financial forecast and wondered what it could like for personal finances. Well here is a quick snapshot below

This is my tax assets plan (by tax type)

This is my simple cash flow plan

It is difficult to rise your ahead above the daily grind to ask the important questions about why you are doing it all. I can’t stress though, that it is an important habit. You don’t want to be an unhappy rich person. There is one quote that has always stuck with me from Steve Jobs

“Being the richest man in the cemetery doesn’t matter to me. Going to bed at night saying we’ve done something wonderful… that’s what matters to me.”

As someone who lost his father to cancer when he was 53, this really resonated with me. This is why you need to plan the great life, don’t suffer the long life

I admitted that I could fail and just got back on the wagon

The last point is really important to understand. Most entrepreneurs understand that “failure” is a required element of success. I see this in most facets of life and business apart from personal finance. People don’t trust themselves to make financial decision so that don’t make any financial decisions. I wrote about this previously in Inertia with money is an active decision

Be prepared to fail with your money. Be prepared to overspend but at least give it a go, use some of the habits I use for my family and start to build a plan about how to get “what you really want” . Don’t forget the minute you build a financial plan and start it, it is obsolete as life changes and you must evolve it all the time but if you keep asking the right questions and you setup your finances with automation then I genuinely believe that you will succeed.

And if you need any help with the above, remember I do this for a living and help people all the time, so I am sure I could give you a steer in the right direction.